Housing affordability is becoming a big concern in cities across India, with property prices rising faster than people’s incomes. According to the latest Affordability Report by Magicbricks – Housing Affordability in Major Indian Cities (2024), two important factors help us understand how affordable homes really are—the Price to Income (P/I) ratio and the EMI to Income (EMI/I) ratio. In this blog, we’ll break down these factors, see how they affect housing affordability in major cities, and look at the trends that are shaping the market today.

Recognizing Important Affordability Metrics

Price to Income (P/I) Ratio

The Price to Income (P/I) ratio shows how the price of a property compares to the average annual income of a household. It tells us how many years’ worth of income would be needed to buy a home without taking out a loan.

If the P/I ratio is above 5, it usually points to an affordability problem, meaning that the cost of owning a home becomes too high compared to what people earn. In cities with a high P/I ratio, buyers may find it difficult to afford a home without relying heavily on loans.

EMI to Income (EMI/I) Ratio

The EMI to Income ratio reflects the percentage of a household’s monthly income that goes towards repaying home loan EMIs (Equated Monthly Installments). Technically, this ratio should stay below 40-50% to ensure that the borrower can comfortably meet other living expenses. A higher EMI/I ratio may signal overburdened borrowers, making housing financially unfeasible for many.

The Current Affordability Landscape in India

1. Price to Income (P/I) Ratio: A Growing Concern

According to the Housing Affordability in Major Indian Cities (Aug 2024) report, the P/I ratio in Indian cities has seen a significant upward trend in recent years. This metric is a reflection of the growing disparity between rising property prices and slower income growth.

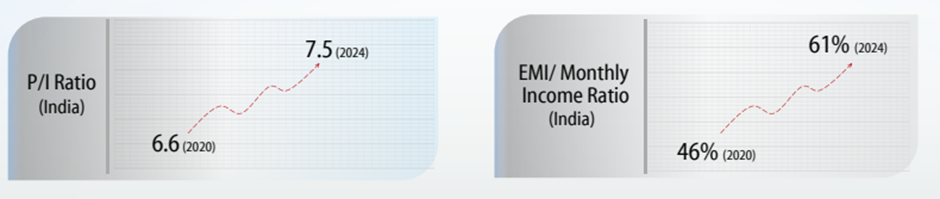

National Average P/I Ratio: The average P/I ratio across India in 2024 has increased to 7.5, up from 6.6 in 2020. This indicates that, on an average, property prices are now nearly 7.5 times the annual household income.

City-Wise Breakdown:

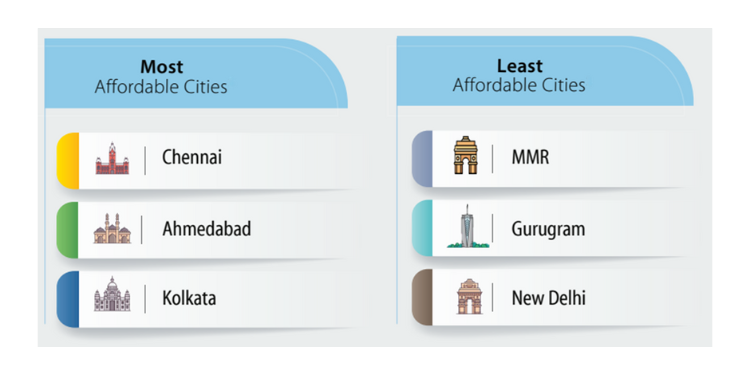

Mumbai Metropolitan Region (MMR): The P/I ratio here has surged to a staggering 14.3, making it one of the least affordable cities for prospective buyers.

Delhi NCR: The P/I ratio is around 10.1, also indicating significant affordability challenges.

Chennai and Ahmedabad: These cities offer relatively better affordability with P/I ratios of 5.1, making them more attractive for potential homeowners.

2. EMI to Income (EMI/I) Ratio: The Burden of Rising EMIs

The EMI/I ratio provides a clear indication of how much of a household’s income is being allocated to repaying home loans. With interest rates on home loans climbing steadily, the EMI/I ratio has been on the rise, further eroding housing affordability.

National Average EMI/I Ratio: The EMI/I ratio in India has risen from 46% in 2020 to 61% in 2024, reflecting the increased cost of borrowing due to rising interest rates.

High Interest Rates Impact: Home loan interest rates have surged from 7.35% in 2020 to 9.1% in 2024, further pushing up EMIs for buyers. As a result, the higher EMI/I ratio indicates that a significant portion of household income is now going toward servicing home loans.

This trend signals a decline in housing affordability, especially in major cities, where the EMI/I ratio has reached concerning levels:

· Mumbai Metropolitan Region (MMR): 116%

· New Delhi: 82%

· Gurugram: 61%

· Hyderabad: 61%

On the other side, cities like Ahmedabad (41%), Chennai (41%), and Kolkata (47%) present a more favorable picture of housing affordability.

3. The Affordability Gap

The report further highlights that between 2020 and 2024, household incomes in major cities grew at a CAGR of 5.4%, while property prices surged by 9.3%. As stated previously, this disparity has further led to weakened affordability.

Why These Metrics Matter

Both the EMI/Income ratio and the Price to Income ratio are important indicators of housing affordability and act as red flags/ warning signs for investors, financial institutions, and purchasers.

For Homebuyers: A higher P/I ratio and EMI/I ratio indicate that homeownership may be financially out of reach for most buyers. This can lead to a higher reliance on home loans, potentially increasing the risk of default.

For Investors: Investors should consider cities with a balanced P/I ratio and EMI/I ratio for stable returns and low market volatility. Cities with high ratios may face slower growth due to affordability constraints.

For Lenders: Financial institutions use these metrics to assess loan risk. A high EMI/I ratio might lead to stricter lending conditions, while a high P/I ratio could reduce the overall demand for housing.

Insights into City-Specific Affordability

Cities such as Chennai, Ahmedabad, and Kolkata are still considerably more inexpensive due to reasonable property costs and lower EMI/I ratios. Cities like Mumbai and Delhi NCR have some of the highest P/I and EMI/I ratios, and prices are continuing to rise due to high demand and limited availability.

The Road Ahead for Housing Affordability

While current trends in housing affordability are alarming, there are various measures that could alleviate the situation.

Government Schemes: Programs like the Pradhan Mantri Awas Yojana (PMAY) aim to provide affordable housing for all, potentially lowering the P/I ratio in the long term.

Price Stabilization: Developers are increasingly turning their attention to affordable housing projects, which could help bring down the average property prices in the coming years.

Income Growth: With the Indian economy expected to continue growing, household incomes are likely to rise, which could gradually improve the P/I ratio.

Conclusion

In conclusion, the Price to Income ratio and the EMI to Income ratio are among the most important indicators of housing affordability, and both these metrics signify the challenges faced by potential homebuyers in urban India. As the Housing Affordability in Major Indian Cities (2024) report shows, cities like Mumbai and Delhi NCR are becoming increasingly unaffordable, whereas cities like Chennai and Ahmedabad offer comparatively better opportunities for homebuyers.

An understanding of these measures and their implications can help homebuyers, investors, and policymakers make informed decisions, ensuring that the dream of homeownership remains attainable for more people in India.