Are You Paying More Tax Than You Should?

Imagine two colleagues – Rahul and Priya – both earning ₹12 lakh per year. Come March, Rahul pays ₹1.8 lakh in taxes. Priya pays just ₹60,000. Same salary, very different tax bills. The difference? Priya understands tax avoidance and puts it to work for her every financial year.

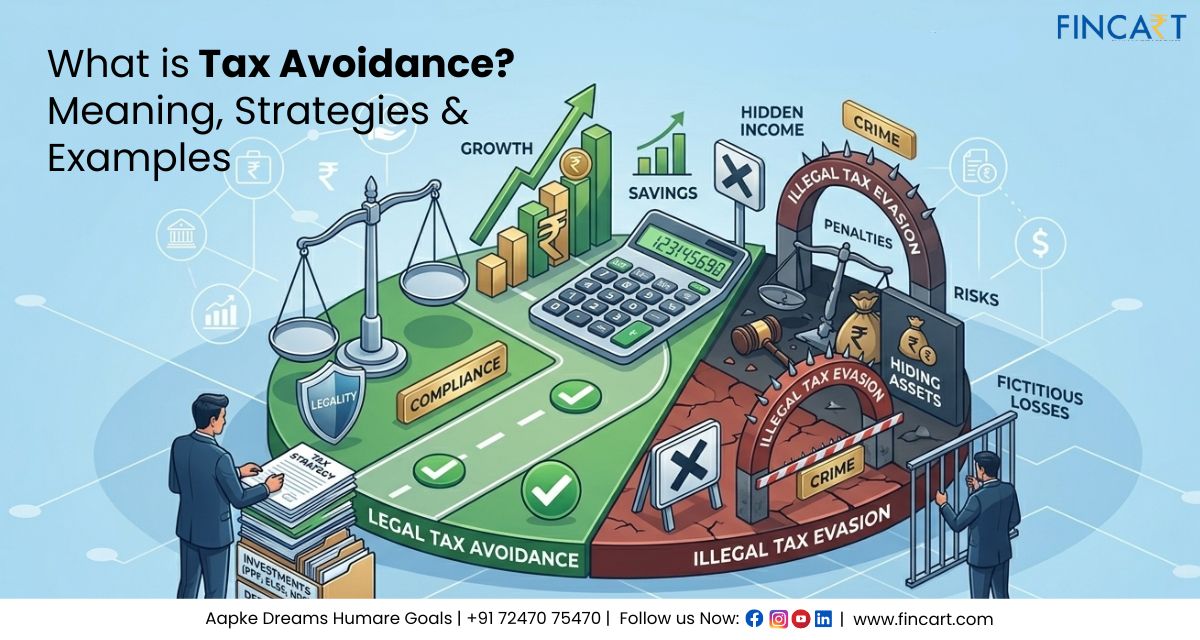

Tax avoidance is not a loophole for the wealthy or a grey-area trick. It is a perfectly legal, government-endorsed approach to reducing how much tax you owe.

Yet, despite its importance, tax avoidance remains widely misunderstood. Many people either confuse it with the illegal practice of tax evasion or miss out on legitimate savings simply because they do not know where to begin.

In this blog, Fincart breaks down everything you need to know: what it actually means, the most effective strategies you can use right now, and how it differs from tax evasion.

What is Tax Avoidance? Meaning and Definition

It refers to the legal practice of arranging your finances and investments in a way that reduces your total tax liability. Unlike cheating the system, tax avoidance works entirely within the framework of the Income Tax Act, 1961 – using the exemptions, deductions, and provisions that Parliament has built into the law for taxpayers to use.

In simple terms, It means you are not paying more tax than the law requires you to. Every deduction you claim, every allowance you use, and every exempt investment you make is a form of tax avoidance – and it is completely acceptable.

It is important to distinguish tax avoidance from routine tax planning. Tax planning is the broader process of structuring your finances across the year to align with your financial goals, while also keeping tax efficiency in mind. Tax avoidance is more specific – it focuses directly on the strategies and provisions that lower your tax bill.

For example, a salaried employee who contributes ₹1.5 lakh to a Public Provident Fund (PPF) to claim a deduction under Section 80C is practising tax avoidance. An employer who structures employee salaries to include House Rent Allowance (HRA) is also facilitating tax avoidance – both actions are encouraged by the Income Tax Department.

For individual taxpayers in India, It is entirely straightforward, widely practised, and strongly recommended. Every legitimate rupee you save through tax avoidance is a rupee that stays in your hands – to save, invest, or spend on the things that matter to you.

Top Tax Avoidance Strategies for Indian Taxpayers

India’s Income Tax Act provides several powerful avenues for tax avoidance. Here are the most effective, practical strategies you can start using today:

1. Maximise Section 80C Deductions (Up to ₹1.5 Lakh)

You can claim deductions of up to ₹1.5 lakh per year by investing in instruments such as:

• Employee Provident Fund (EPF) contributions

• Public Provident Fund (PPF)

• Equity Linked Savings Scheme (ELSS) mutual funds

• National Savings Certificate (NSC)

• Life insurance premium payments

2. Claim Home Loan Benefits Under Sections 80C and 24(b)

If you have a home loan, you can claim a deduction of up to ₹1.5 lakh on principal repayment under Section 80C and up to ₹2 lakh on interest paid under Section 24(b). This makes a home loan one of the most powerful avoidance tools available to Indian taxpayers.

3. Use Health Insurance for Section 80D Deductions

Paying premiums for health insurance qualifies for deductions under Section 80D – up to ₹25,000 for yourself, spouse, and children, and an additional ₹25,000 (or ₹50,000 for senior citizens) for your parents. This strategy delivers both financial protection and significant avoidance benefits.

4. Optimise Your Salary Structure

If you are salaried, ask your employer whether your CTC can be restructured to include components like HRA (House Rent Allowance), LTA (Leave Travel Allowance), meal coupons, and phone/internet reimbursements. These components are either fully or partially exempt from tax, making salary restructuring one of the most immediate forms of avoidance available.

5. Invest in National Pension System (NPS) Under Section 80CCD

Maximum Limit:

- Assessee’s own contribution under section 80CCD(1) – Up to 10% of basic pay can be claimed as a deduction.

- Combined limit of deduction under section 80C, 80CCC, and 80CCD(1) – Rs. 1.5 lakhs

- Additional deduction under section 80CCD(1B) – Rs. 50,000

- Under section 80CCD(2), an employer’s contributions up to 10% of the basic pay can be claimed as a deduction.

Tax Avoidance vs. Tax Evasion: Understanding the Critical Difference

The single most important thing to understand about this is what it is not. It is not tax evasion, and confusing the two can land you in serious legal trouble.

Comparison: Tax Avoidance vs. Tax Evasion

| Basis | Tax Avoidance | Tax Evasion |

| Definition | Reducing tax liability using legal provisions of the Income Tax Act. | Deliberately hiding income or fabricating information to escape taxes. |

| Legality | Completely legal and compliant. | Illegal and punishable under Indian law. |

| Intent | To minimise tax outgo through smart, permitted financial planning. | To deceive the Income Tax Department by misrepresenting facts. |

| Methods | Investing in PPF, ELSS; claiming Section 80C, 80D, 24(b) deductions; using HRA exemptions. | Under-reporting income, creating false receipts, hiding cash transactions. |

| Example | Priya invests ₹1.5 lakh in PPF to claim Section 80C deduction fully. | Raj shows ₹50,000 in fake donations to inflate his deduction claims. |

| Consequence | No legal repercussions when done within permitted limits. | Heavy fines, back-tax recovery, interest, and possible imprisonment. |

When Does Tax Avoidance Become Legally Questionable?

While most forms of individual tax avoidance are perfectly acceptable. The IT Department scrutinises arrangements when large corporations use highly aggressive structures, sometimes exploiting technical loopholes rather than the spirit of the law, to dramatically reduce their tax liability. Even so, as long as such arrangements remain within legal boundaries, they technically qualify as tax avoidance rather than tax evasion.

The safest way to practise it is to work with a qualified tax consultant or experienced planner. A good tax planner ensures every strategy you use is both legitimate and correctly documented – protecting you from scrutiny while maximising your savings.

Conclusion: Use Tax Avoidance Wisely – and Legally

It is one of the smartest financial habits any Indian taxpayer can develop. By using the deductions, exemptions, and provisions the Income Tax Act provides, you reduce your tax burden without breaking any rules or putting yourself at legal risk.

FAQs

Is tax avoidance legal in India?

Yes, it is completely legal. It involves using provisions in the Income Tax Act, like Section 80C, 80D, and home loan deductions, to reduce your tax liability. It is distinct from tax evasion, which is illegal.

What is the difference between tax avoidance and tax planning?

Tax planning is the broader process of organising your finances to minimise tax liability over time. It is a component of planning; it specifically refers to using legal provisions and exemptions to reduce the tax you owe in a given year.

Tax avoidance vs Tax Evasion

Avoidance is reducing tax liability using legal provisions of the Income Tax Act. Whereas Tax Evasion is deliberately hiding income or fabricating information to escape taxes.

Can salaried employees practise tax avoidance?

Absolutely. Salaried employees can use HRA exemptions, LTA, Section 80C investments (ELSS, PPF, life insurance), Section 80D health insurance premiums, and NPS contributions under 80CCD(1B), all of which are powerful avoidance tools.

How much tax can I save through tax avoidance under Section 80C?

Under Section 80C, you can claim deductions of up to ₹1.5 lakh per year. For someone in the 30% tax bracket, this alone can save up to ₹46,800 annually (including cess). Combining 80C with 80D and NPS can push total savings significantly higher.

Is there a difference between tax avoidance and tax exemption?

Yes. A tax exemption means certain income is entirely excluded from tax (e.g., HRA, agricultural income, life insurance maturity proceeds under Section 10(10D)). It is the strategic use of both exemptions and deductions together to minimise overall tax liability.