Indian investors are facing a complex environment—volatile equity markets, rising interest rates, inflation concerns, and global uncertainty. Traditional single-asset investing is no longer enough. This is where a multi asset allocation fund becomes highly relevant.

Within the first few years of investing, many people realize that returns alone don’t define success—risk management does. A multi asset allocation fund aims to solve this by spreading investments across equity, debt, gold, and other asset classes, reducing dependency on any single market.

What Is a Multi Asset Allocation Fund? (Definition & Meaning)

A multi asset allocation fund is a type of mutual fund that invests in at least three different asset classes, with equity and debt being mandatory, and a third asset such as:

- Gold / Commodities

- REITs / InvITs

- International equities

As per regulations by SEBI, each asset class must have a minimum allocation of 10%.

Simple Definition

A multi asset allocation fund diversifies investments across multiple asset classes to balance risk and returns across market cycles.

How Multi Asset Allocation Funds Work

These funds follow dynamic asset allocation, meaning:

- Equity exposure increases during market corrections

- Debt allocation rises during high interest rate periods

- Gold acts as a hedge during inflation or geopolitical stress

Fund managers actively rebalance the portfolio based on:

- Market valuations

- Macroeconomic indicators

- Interest rate trends

- Global risk sentiment

This professional management is particularly valuable for investors who don’t want to track markets daily.

Types of Assets Used in Multi Asset Allocation Funds

1. Equities (Stocks)

The core growth engine of most multi-asset funds.

- Domestic equities – shares listed on local stock exchanges (e.g., NSE/BSE in India)

- International/Global equities – exposure to US, European, or emerging market stocks

- Large-cap, mid-cap, small-cap – different risk-return profiles within equities

- Sectoral exposure – IT, banking, pharma, etc., held either directly or via ETFs

2. Fixed Income (Debt)

Provides stability and regular income.

- Government securities (G-Secs) – sovereign bonds, lowest credit risk

- Corporate bonds – higher yield but more credit risk

- Money market instruments – T-bills, commercial paper, short-duration instruments

- PSU bonds – issued by public sector undertakings

3. Gold

A classic hedge against inflation and currency depreciation.

- Held via Gold ETFs, Sovereign Gold Bonds (SGBs), or physical gold units

- Tends to perform well during market stress or geopolitical uncertainty

4. Real Estate

- Accessed through REITs (Real Estate Investment Trusts) — listed instruments that own commercial/retail properties

- Provides rental income + potential capital appreciation without direct property ownership

5. Commodities

- Includes silver, oil, agricultural commodities

- Usually accessed via commodity ETFs or futures

- Acts as an inflation hedge and diversifier

6. Cash & Cash Equivalents

- Held to manage liquidity and deploy during market corrections

- Includes liquid funds, overnight funds, and short-term deposits

7. International Assets / Global Funds

- Exposure to foreign equities or bonds for geographic diversification

- Reduces dependence on a single country’s economic cycle

8. InvITs (Infrastructure Investment Trusts)

- Similar to REITs but focused on infrastructure assets like roads, power lines, pipelines

- Offer regular distributions + growth potential

How Allocation Works

| Asset Class | Role in Portfolio | Risk Level |

| Equities | Growth | High |

| Debt | Stability & Income | Low–Medium |

| Gold | Hedge / Safe Haven | Medium |

| REITs/InvITs | Income + Diversification | Medium |

| Commodities | Inflation Hedge | Medium–High |

| Cash | Liquidity Buffer | Very Low |

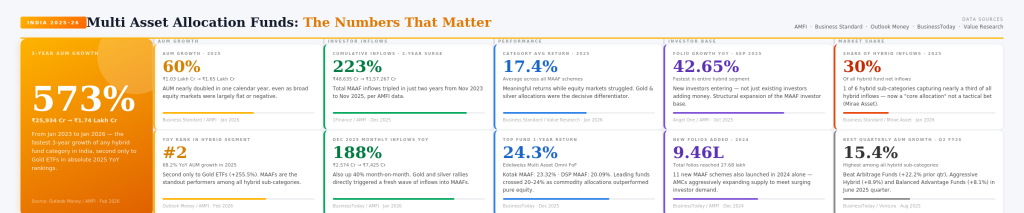

Why Multi Asset Allocation Funds Are Gaining Popularity in India

Multi-asset allocation funds have seen significant growth in AUM and investor interest in India over recent years. Here’s a comprehensive explanation of the driving factors:

1. Regulatory Push by SEBI

- SEBI’s categorization and rationalization of mutual fund schemes (2017) formally defined multi-asset funds as those investing in at least 3 asset classes with minimum 10% in each

- This gave investors a clear, regulated framework to trust

- SEBI’s investor awareness programs have also increased general financial literacy

2. Volatility in Equity Markets

- Post-COVID market swings (2020–2023) demonstrated how single-asset portfolios can be devastated quickly

- Investors who suffered losses in pure equity funds became more risk-conscious

- Multi-asset funds offered a smoother ride — when equities fell, gold or debt cushioned the blow

- This real-world experience converted many investors to the multi-asset philosophy

3. Rise of the Indian Middle Class & First-Time Investors

- India’s growing middle class is increasingly surplus-income generating and looking beyond FDs

- Many first-time mutual fund investors find multi-asset funds less intimidating — one fund, many assets

- The “one-stop solution” appeal is strong for those who don’t want to manage multiple funds

4. Gold’s Cultural & Financial Appeal in India

- Indians have a deep cultural affinity for gold — multi-asset funds satisfy this by including gold ETFs/SGBs within the portfolio

- Gold allocation provides both emotional comfort and financial hedge, especially during rupee depreciation or geopolitical tensions

- Having gold in a paper/digital form (within the fund) removes storage and purity concerns

5. Tax Efficiency

- Multi-asset funds (with 65%+ equity) are taxed as equity funds — LTCG at 12.5% after ₹1.25 lakh exemption (post Budget 2024)

- This is far more tax-efficient than holding debt funds, gold bonds, and equity separately

- Rebalancing within the fund does not trigger capital gains tax for the investor — the fund manager can shift allocations freely without tax consequences to the unitholder

6. Automatic Rebalancing — Discipline Without Effort

- Most retail investors fail to rebalance their own portfolios due to inertia, emotions, or lack of knowledge

- Multi-asset funds do this automatically and professionally

- When equities are overvalued, the fund trims equity and moves to debt/gold — enforcing buy low, sell high discipline on behalf of investors

7. Macroeconomic Uncertainty

- Global factors — US Fed rate cycles, geopolitical conflicts, inflation spikes, dollar strength — have made single-asset investing riskier

- Indian investors are increasingly aware that no single asset class outperforms every year

- Multi-asset funds hedge against this uncertainty across cycles

8. SIP Culture & Long-Term Investing Trend

- India’s SIP inflows crossed ₹20,000 crore/month — showing deepening mutual fund culture

- Multi-asset funds are ideal for SIP investors seeking stable long-term compounding

- Financial advisors increasingly recommend them as core portfolio holdings for moderate-risk investors

9. Underperformance of Traditional Safe Havens

- Fixed Deposits offer returns that barely beat inflation after tax

- Real estate requires large capital, is illiquid, and has regulatory complications

- Physical gold has storage/safety risks

- Multi-asset funds offer better risk-adjusted returns than these traditional options, attracting investors who are “graduating” from FDs and physical assets

10. Proliferation of Fund Options & AMC Competition

- Major AMCs — HDFC, ICICI Prudential, Nippon, SBI, Kotak — have launched well-performing multi-asset schemes

- Strong track records (especially during 2020–2024 volatile periods) have built investor confidence

- Distribution through Zerodha, Groww, Paytm Money has made access easier than ever

Multi Asset Allocation Fund vs Other Mutual Funds

| Feature | Multi Asset Allocation Fund | Equity Fund | Debt Fund | Other Hybrid Fund |

| Asset Classes | 3 or more | Equity only | Debt only | Equity and debt |

| Risk Level | Moderate | High | Low | Moderate |

| Active Rebalancing between asset classes | Yes | No | No | Yes, but limited |

| Inflation Protection | Higher | Medium | Low | Medium |

| Ideal For | Long-term stability | Aggressive growth | Capital preservation | Balanced growth |

Benefits of Investing in a Multi Asset Allocation Fund

Multi-asset allocation funds offer a compelling combination of advantages that make them suitable for a wide range of investors. Here is a detailed breakdown of all the key benefits:

1. Diversification Across Asset Classes

The most fundamental benefit — spreading risk across multiple assets.

- A single fund invests across equities, debt, gold, REITs, commodities etc.

- When one asset class underperforms, others may compensate and stabilize returns

- Reduces concentration risk — the danger of being overly exposed to one market

- Achieves what would otherwise require multiple separate funds and accounts

2. Professional & Dynamic Asset Allocation

Fund managers actively manage the portfolio — not a static mix.

- Experienced fund managers continuously monitor markets, valuations, and macro trends

- They shift allocations dynamically — increasing equity when markets are attractive, moving to debt/gold when equity is expensive or risky

- Uses quantitative models + qualitative judgment to time asset rotation

- Retail investors get institutional-grade portfolio management without needing expertise themselves

3. Automatic Rebalancing — Without Tax Consequences

One of the most underrated benefits of multi-asset funds.

- Fund manager rebalances the portfolio (e.g., trims equity after a rally, adds debt) without triggering capital gains tax for the investor

- If an individual investor did this themselves — selling equity funds to buy gold — it would attract capital gains tax

- Within the fund, this rebalancing is seamless and tax-neutral for the unitholder

- Enforces buy low, sell high discipline automatically

4. Risk-Adjusted Returns

Better returns per unit of risk taken — the true measure of investing efficiency.

- Multi-asset funds typically show lower volatility (measured by standard deviation) than pure equity funds

- Sharpe Ratio (return per unit of risk) is often superior to single-asset class funds over long periods

- Investors experience fewer heart-stopping drawdowns, making it easier to stay invested

- Particularly beneficial during bear markets and sideways markets

5. Tax Efficiency

Structured smartly, multi-asset funds can be highly tax-efficient.

- Funds with 65%+ equity allocation are classified as equity funds for taxation:

- STCG: 20% (held less than 1 year)

- LTCG: 12.5% after ₹1.25 lakh annual exemption (held more than 1 year)

- This is significantly better than holding debt funds (taxed at slab rate) or physical gold separately

- No tax on internal rebalancing — the fund’s switching between assets does not create any tax liability for the investor

- Single tax event instead of multiple — simplifies tax filing

6. Convenience & Simplicity

A truly “all-in-one” investment solution.

- Investor needs to track just one fund instead of managing equity, debt, gold, and REIT funds separately

- Eliminates the complexity of deciding how much to allocate to each asset class

- Single SIP, single statement, single KYC covers all asset classes

- Ideal for busy professionals and first-time investors who want a complete solution without deep market knowledge

- Reduces decision fatigue — one of the biggest enemies of good investing

7. Wealth Preservation During Market Downturns

Multi-asset funds are designed to protect capital during stress.

- Debt and gold components act as shock absorbers during equity market crashes

- Historical data shows multi-asset funds typically fall less during bear markets than pure equity funds

- Faster recovery of invested capital compared to single-asset equity portfolios

- Particularly important for conservative-to-moderate risk investors who cannot afford large drawdowns

8. Inflation Hedging

Protection against the silent wealth destroyer — inflation.

- Equity component grows wealth above inflation over the long term

- Gold is a proven inflation hedge — historically rises when real interest rates fall

- Real assets (REITs, commodities if included) provide additional inflation protection

- Together, these create a portfolio that is structurally resistant to purchasing power erosion

9. Suitable Across Market Cycles

Multi-asset funds are designed to perform in all seasons.

| Market Condition | Asset That Helps |

| Bull Market (Rising Equities) | Equity component drives returns |

| Bear Market (Falling Equities) | Debt & Gold provide stability |

| High Inflation | Gold & commodities hedge |

| Low Interest Rate Environment | Equity and REITs benefit |

| Geopolitical Uncertainty | Gold acts as safe haven |

| Economic Recovery | Equity leads the rebound |

10. Behavioral Benefits — Staying Invested

Perhaps the most overlooked but most powerful benefit.

- Lower volatility means investors are less likely to panic and exit during market falls

- Smoother return journey improves investor psychology and staying power

- Studies show that investor returns are far lower than fund returns because people exit at the wrong time

- Multi-asset funds, by reducing volatility, help investors stay the course and actually realize the long-term returns the fund generates

- SIP in a multi-asset fund leads to consistent, emotion-free investing

11. Access to Asset Classes Otherwise Difficult to Invest In

Multi-asset funds democratize access.

- REITs and InvITs — require significant capital and knowledge to invest directly; the fund handles this

- International equities — complex to invest in directly; fund provides this exposure

- Commodities — futures trading is complex for retail investors; fund accesses this professionally

- Even gold via SGBs or ETFs — the fund manages this optimally

12. Ideal for Goal-Based Investing

Multi-asset funds align well with real-life financial goals.

- Medium to long-term goals (5–15 years) — child’s education, retirement, home purchase

- The equity component drives long-term growth toward the goal

- The debt and gold components protect accumulated corpus as the goal approaches

- Works excellently as a single-fund retirement solution for moderate risk investors

Risks and Limitations You Should Know

No investment is risk-free.

Potential Drawbacks:

- Lower returns during strong bull markets compared to pure equity funds

- Fund manager’s asset allocation decisions impact performance

- Expense ratios may be slightly higher

However, for most investors, the stability trade-off is worth it.

Who Should Invest in Multi Asset Allocation Funds?

This fund category is suitable for:

- First-time mutual fund investors

- Salaried professionals

- Investors with moderate risk appetite

- Those without time to rebalance portfolios

A qualified mutual fund advisor can assess suitability based on your goals and risk tolerance.

How to Choose the Best Multi Asset Allocation Fund in India

Key Evaluation Factors:

- Asset Allocation Strategy – Check equity-debt-gold balance and whether that aligns with the current market outlook

- Fund Manager Track Record

- Consistency Across Market Cycles

- Expense Ratio

- Fund House Reputation

Avoid selecting funds based solely on past returns.

Role of a Mutual Fund Consultant or Mutual Fund Advisor

A professional mutual fund consultant helps you:

- Align funds with financial goals

- Avoid emotional investing

- Optimize asset allocation

- Plan taxes efficiently

For investors managing multiple goals, expert guidance adds significant value.

Taxation of Multi Asset Allocation Funds in India

Tax treatment of hybrid funds depends on equity exposure:

- Equity ≥ 65% → Taxed like equity funds

- Equity < 65% → Taxed like debt funds

Recent changes have made taxation more nuanced, making advisory support important.

Real-World Example: Portfolio Allocation Across Market Cycles

Scenario:

An investor allocates ₹10 lakh into a multi asset allocation fund.

| Asset | Allocation |

| Equity | 45% |

| Debt | 35% |

| Gold | 15% |

| REITs | 5% |

During a market crash:

- Equity falls

- Debt stabilizes

- Gold rises

Net portfolio impact is significantly cushioned.

Step-by-Step Guide to Investing in a Multi Asset Allocation Fund

Step 1: Define Your Financial Goal

Every investment journey must begin with a clear purpose. Ask yourself — what am I investing for? It could be a child’s education, retirement, home purchase, or wealth creation. Once the goal is identified, calculate the future value of that goal accounting for inflation, determine your time horizon, and work backwards to find the monthly SIP amount needed. Multi-asset funds work best for goals that are 5 years or more away.

Step 2: Assess Risk Tolerance

Understanding how much risk you can emotionally and financially handle is critical. Risk tolerance has two sides — your financial capacity (income stability, liabilities, dependents) and your emotional capacity (can you stay calm when your portfolio falls 20–25% temporarily?). Multi-asset funds suit conservative to moderate risk investors best, as the debt and gold components cushion equity volatility and reduce the severity of drawdowns during market corrections

Step 3: Shortlist Funds

Not all multi-asset funds are equal. Evaluate funds on 5-year rolling returns (consistency matters more than one-year performance), expense ratio (prefer Direct Plans below 1%), fund manager experience, AUM stability (₹1,000 crore+), and downside protection during past market crashes like March 2020. Use platforms like Value Research or Morningstar for objective comparison. Narrow your selection down to 1 or 2 well-researched funds — over-diversifying across too many funds defeats the purpose.

Step 4: Choose SIP or Lump Sum

For salaried investors with regular income, SIP is the ideal choice — it automates investing, removes market timing stress, and benefits from rupee cost averaging by buying more units when markets are low. For those with a large one-time amount (bonus, inheritance), consider an STP (Systematic Transfer Plan) — park the money in a liquid fund and transfer monthly into the multi-asset fund. Invest lump sum directly only when markets have corrected significantly.

Step 5: Review Annually with a Mutual Fund Advisor

Once invested, review your portfolio once a year with a SEBI-registered advisor. Check if the fund is beating its benchmark consistently, whether your personal financial situation has changed (income, liabilities, new goals), and if your SIP amount needs stepping up. A good advisor also helps with tax planning — harvesting up to ₹1.25 lakh LTCG tax-free annually — and prevents panic-driven exits during market downturns, which is one of the biggest destroyers of long-term wealth.

FAQ Section

1. Is a multi asset allocation fund good for beginners?

Yes, it offers diversification and professional management, making it ideal for new investors.

2. How many years should I stay invested?

At least 3 years for optimal results.

3. Is SIP better than lump sum?

SIP helps average costs and reduce timing risk.

4. Can I invest without a mutual fund advisor?

Yes, but guidance improves fund selection and discipline.

5. Are multi asset funds safer than equity funds?

They are generally less volatile but not risk-free.

6. Do multi asset allocation funds give regular income?

Some offer dividend options, but growth plans with STP are preferred for tax optimisation.