For salaried individuals living in rented accommodation, House Rent Allowance (HRA) is one of the most valuable tax-saving tools available under the Indian Income Tax Act. Yet, a surprisingly large number of employees either claim it incorrectly or leave money on the table simply because the rules feel confusing.

This guide breaks down everything about HRA exemption, including how it works, how to calculate it, what documents are needed, and how to avoid common mistakes.

What Is HRA and Why Does It Matter?

HRA, or House Rent Allowance, is a component of salary that employers pay to help cover rental expenses. Under Section 10(13A) of the Income Tax Act, a portion of this allowance can be claimed as exempt from tax, meaning that portion does not get added to taxable income.

This benefit is available only to salaried employees who actually pay rent for their accommodation. Employees who own the house they live in cannot claim this exemption, even if the employer pays an HRA component as part of the salary structure.

Who Can Claim HRA Exemption?

HRA exemption is available to individuals who meet all of the following conditions:

- Salaried employment (this benefit does not apply to self-employed individuals under the old tax regime)

- HRA is part of the employer’s salary structure

- Rent is actually paid for the house being occupied

- Taxes are being filed under the old tax regime

Under the new tax regime, HRA exemption is not available. The new regime offers lower tax slabs but removes most deductions and exemptions, including HRA. Given this trade-off, many salaried individuals with significant rent expenses find the old regime more beneficial. A tax consultant can help model both scenarios and identify which one results in greater savings.

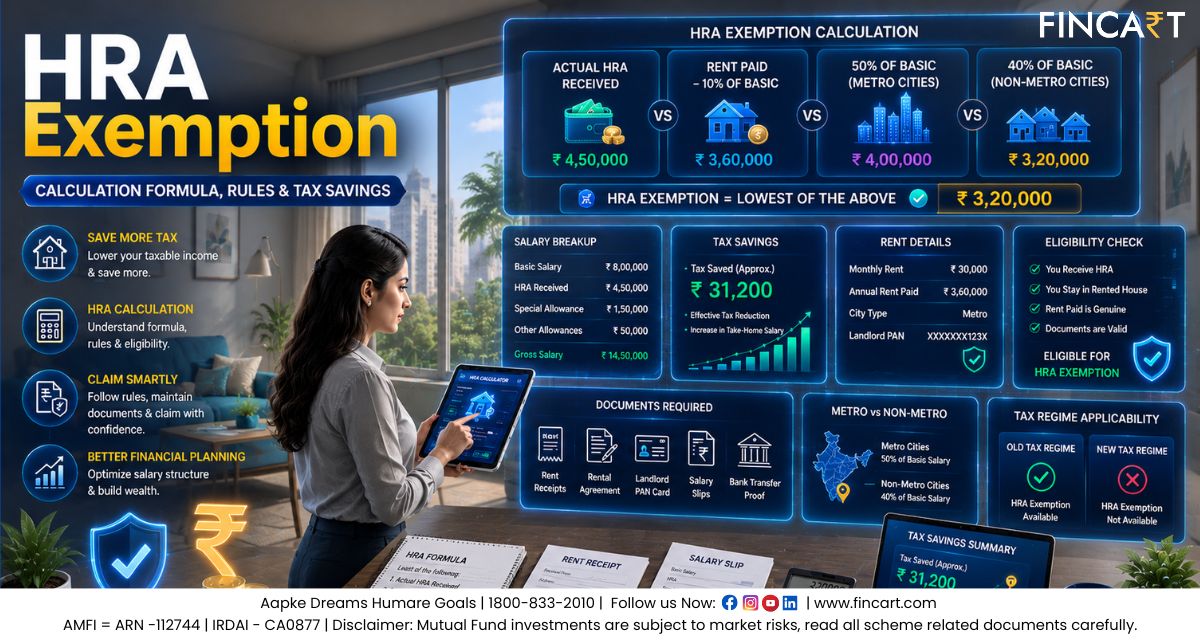

The Three-Part Formula: How HRA Exemption Is Calculated

The exemption is not simply the full HRA paid by the employer. The Income Tax Department uses a specific formula: the exemption equals the lowest of the following three amounts:

- Actual HRA received from the employer during the year

- 50% of salary for metro city residents (Delhi, Mumbai, Kolkata, Chennai), or 40% of salary for non-metro city residents

- Actual rent paid minus 10% of salary

Whichever of these three figures is lowest becomes the HRA exemption for the year. You must add any remaining HRA to your taxable income.

Note that for this formula, “salary” means Basic Salary + Dearness Allowance (DA). It does not include HRA itself, special allowances, or other components.

A Step-by-Step Calculation Example

Assume the following monthly figures:

- Basic Salary: ₹50,000

- Dearness Allowance (DA): ₹5,000

- HRA received from employer: ₹20,000

- Monthly rent paid: ₹18,000

- City: Delhi (metro)

Step 1: Calculate “Salary” for HRA purposes

Basic + DA = ₹50,000 + ₹5,000 = ₹55,000 per month

Annual salary = ₹55,000 × 12 = ₹6,60,000

Step 2: Calculate the three figures on an annual basis

- Actual HRA received

₹20,000 × 12 = ₹2,40,000 - 50% of salary (metro city)

50% × ₹6,60,000 = ₹3,30,000 - Actual rent paid minus 10% of salary

Annual rent = ₹18,000 × 12 = ₹2,16,000

10% of salary = ₹66,000

₹2,16,000 − ₹66,000 = ₹1,50,000

Step 3: Pick the lowest

The lowest among ₹2,40,000, ₹3,30,000, and ₹1,50,000 is ₹1,50,000.

This means ₹1,50,000 is exempt from tax. You must add the remaining ₹90,000 (₹2,40,000 − ₹1,50,000) to your taxable income.”

What Counts as a Metro City?

For HRA exemption purposes, only four cities qualify as metro cities, giving employees the 50% threshold instead of 40%:

- Delhi (the official definition only covers Delhi city. NCR towns like Gurgaon, Noida, Faridabad, and Ghaziabad may not qualify; employers typically clarify this)

- Mumbai (including Thane and Navi Mumbai)

- Kolkata

- Chennai

Residents of Bengaluru, Hyderabad, Pune, Ahmedabad, or any other city fall under the 40% threshold, even though these are major economic centres. This is a common misconception that leads to incorrect claims.

Rent Receipts and Documentation: What You Actually Need

Many employees assume that simply informing their employer about rent payments is sufficient. It is not. You need the following documentation to support an HRA claim:

Rent receipts are the primary proof. They must include:

- Name of the tenant

- Name and signature of the landlord

- Address of the rented property

- Amount of rent paid

- Period covered (month and year)

- Revenue stamp (for receipts above ₹5,000 per receipt, though most businesses now accept digital receipts)

PAN of the landlord is mandatory if annual rent exceeds ₹1,00,000 (i.e., more than ₹8,333 per month). If the landlord does not have a PAN, a written declaration to that effect must be provided instead.

You don’t always need a rent agreement, but tax authorities strongly recommend maintaining one as supporting evidence.

Rent paid to a parent while living in their house also qualifies for HRA exemption — but the parent must declare that rental income in their own tax return, and the arrangement must be supported by a proper agreement and a clear payment trail.

Common Mistakes That Lead to Rejected Claims

HRA claims look simple on the surface, but a handful of recurring errors cause taxpayers to either lose the exemption entirely or face notices from the Income Tax Department. Being aware of these pitfalls before filing can save a significant amount of trouble.

1. Claiming HRA while also claiming home loan benefits on a property in the same city

This is a grey area. Both HRA and home loan deductions can be claimed simultaneously if the owned property is in a different city from where the employee works and lives on rent. But owning a house in the same city while renting elsewhere can attract scrutiny from the tax department. This is precisely the kind of situation where professional tax consulting services prove useful as even a small misstep here can lead to a demand notice.

2. Missing the employer’s internal deadline for submitting investment proofs

When rent receipts are not submitted on time, TDS gets deducted at a higher rate. The exemption can still be claimed when filing the ITR, but the taxpayer then has to wait for a refund rather than avoiding the deduction at source.

3. Paying rent in cash without documentation

Rent should always be paid via bank transfer, UPI, or cheque. Cash payments are difficult to prove and may not hold up under scrutiny.

4. Claiming a rent figure that does not match receipts

If rent receipts show ₹17,500 per month but the claim states ₹20,000, the mismatch is a red flag. You must ensure your claim reflects exactly what you paid.

5. Applying a single set of figures for the full year when circumstances changed mid-year

A change in city, employer, or rent amount requires a period-wise calculation. Many taxpayers incorrectly apply uniform figures for the entire financial year in such situations.

Section 80GG: HRA for Those Not Covered by Section 10(13A)

Self-employed individuals or salaried employees whose employer does not include HRA in the salary structure are not entirely without options. Section 80GG allows a deduction for rent paid, subject to certain conditions:

- The taxpayer, their spouse, or minor children must not own any residential property at the place of work

- No employer should provide HRA.

- You must file Form 10BA declaring the rent payment.

The deduction under Section 80GG is the lowest of:

- ₹5,000 per month (₹60,000 per year)

- 25% of total income

- Actual rent paid minus 10% of total income

This is significantly more restricted than the standard HRA exemption but provides at least some relief for those outside the salaried bracket.

HRA in the Context of New vs. Old Tax Regime (2025–26 and 2026)

Under the new tax regime, which became the default from FY 2023–24 onwards, HRA exemption is not available. The new regime carries lower tax rates but eliminates most exemptions and deductions including HRA, LTA, Section 80C investments, and more.

The optimal regime depends entirely on the individual’s salary structure and actual deductions. Tax consulting services can run this comparison quickly and help make the right call before the financial year ends.

How to Claim HRA Exemption When Filing the ITR

When the employer has already accounted for HRA exemption, the figure reflects in taxable salary automatically via Form 16. The key step is to verify the figure when filing.

If your employer hasn’t adjusted for HRA, or if you couldn’t submit receipts on time, here’s how to claim HRA exemption while filing ITR:

- In the ITR form, go to the Salary Schedule

- Under “Allowances exempt under Section 10”, enter the calculated HRA exemption under Section 10(13A)

- This reduces gross salary and, therefore, taxable income

- Keep rent receipts and landlord PAN ready in case of scrutiny

It is worth cross-checking the figure on Form 16 (Part B) against an independent calculation. Errors in employer calculations do occur, and the responsibility to file correctly rests with the individual taxpayer, not the employer.

Conclusion

HRA exemption remains one of the most accessible and impactful tax-saving tools for salaried individuals in India. Once you understand the three-part formula, the calculation becomes straightforward, and you can manage the documentation requirements with a little organisation. The key is to claim accurately, maintain a clear paper trail, and revisit the old versus new regime comparison every financial year. For situations involving mid-year job changes, family rent arrangements, or simultaneous home loan claims, speaking with a tax consultant ensures the claim holds up under scrutiny and delivers the maximum legitimate benefit.

Frequently Asked Questions (FAQs)

Q1. How do you calculate HRA exemption?

HRA exemption is the lowest of three amounts: actual HRA received from the employer, 50% of basic salary for metro city residents (40% for non-metro), and actual rent paid minus 10% of basic salary. The lowest figure among these three is the amount exempt from tax.

Q2. Is HRA exemption available in the new tax regime?

No. HRA exemption is not available under the new tax regime. Only salaried employees who opt for the old tax regime can claim it while filing their income tax return.

Q3. What documents do you need to claim HRA exemption?

The primary documents needed are monthly rent receipts signed by the landlord, a rent agreement, and the landlord’s PAN if annual rent exceeds ₹1,00,000. Rent should ideally be paid via bank transfer or UPI to maintain a verifiable payment trail.

Q4. Can you claim HRA exemption and home loan deduction together?

Yes, both can be claimed simultaneously if the owned property is in a different city from where the employee currently works and lives on rent. Claiming both for the same city can attract scrutiny, so consulting a tax consultant in such cases is advisable.

Q5. What is the HRA exemption limit for metro and non-metro cities?

For metro cities (Delhi, Mumbai, Kolkata, and Chennai) the exemption limit is 50% of basic salary. For all other cities, it is 40% of basic salary. This percentage forms one of the three figures used in the HRA exemption calculation, and the lowest of the three is the final exempt amount.

Disclaimer: This article is intended for informational purposes only and does not constitute tax advice. Tax laws and deadlines are subject to change. Please consult a qualified tax consultant before making any filing decisions.